Decreasing Term Assurance With Critical Illness Cover

When you apply for a mortgage you will be required to get decreasing term coverage. If youre not sure what to do and dont already have a financial adviser you can.

Critical Illness Insurance Brampton Critical Illness Insurance Critical Illness How To Get Money

You can have Decreasing Cover up to 500000 and a total of 500000 across all life insurance policies you have with us.

Decreasing term assurance with critical illness cover. Royal London cant advise you what to do but we can answer any questions you might have about your policy. Many Critical Illness Insurance policies will cover the big three illnesses. Decreasing term life insurance is a type of life insurance policy that pays out less over time.

A Decreasing Cover policy pays out on diagnosis of an illness that has no cure or cannot be cured and which is expected to lead to death within 12 months. When you contact us well explain the advice services we offer and the charges. If an event that is covered takes place the policy pays out a lump sum.

You can add Critical Illness Cover for an extra cost when taking out Life Insurance or Decreasing Life Insurance. Decreasing Term or Mortgage Protection policies as they are often known provide cover that matches the outstanding balance of your mortgageloan and will pay a lump sum that can be used to pay off the remaining balance of your mortgageloan in the event of death andor diagnosis of a critical illness. Often a mortgage lender will insist that you have life insurance with.

A decreasing term assurance policy is usually the same as a mortgage term assurance policy. Once we have paid. This increases your mortgage protection as the policy will pay out not only on death but also if you develop an insurer-specified critical illness.

Decreasing Critical Illness to Protect Your Mortgage. Is diagnosed with one of the critical illnesses specified in your policy document or dies. Decreasing Term Assurance Product Features.

Fixed term of years selected to match your mortgage. We offer four interest rates for mortgage or business decreasing term to help make matching your client needs easier - 5 7 8 and 10. If you make a successful critical illness claim you are not eligible for a subsequent death claim.

Assurance shows that it is an insurance product. Term Assurance with Critical Illness choices. Decreasing Term - Mortgage or Business Protection Calculator.

Peace of mind over a fixed term. Click to open Decreasing term assurance. The term is also fixed.

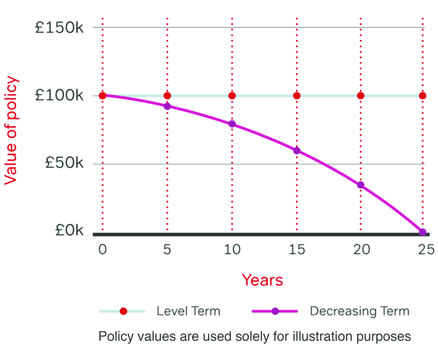

Decreasing Term Assurance to cover a loan is a form of Mortgage Protection. The lump sum reduces each year until the end of the policy term. You specify how long you want the cover to last for when you apply.

No benefit on survival. Most decreasing term life insurance policies come with or allow you to addon terminal and critical illness riders. However this additional protection will increase the cost of your monthly premium.

No relevance to an Interest Only mortgage consider a level term instead May not cover family sufficiently by the time a claim is made. Premiums stay the same for the whole term. With this type of insurance your mortgage loan could be repaid if you were to suffer a serious illness or injury within the policy term but on a decreasing basis which means the cover falls over time alongside your outstanding mortgage.

However if you really want to make sure that your mortgage is paid even if you get critically ill then you can consider adding a decreasing critical illness insurance cover. This calculator can help you to see how much your clients could receive in the event of a claim. Decreasing Term Assurance And Critical Illness Cover What is it.

This would most likely cover you against conditions like a stroke heart attack Parkinsons disease MS Alzheimers disease and more. Decreasing term life insurance with critical illness cover. Term means it has a fixed number of years to run and eventually expires.

Critical illness - this option is usually quite expensive to add but that is because youre more likely to claim against it. It could pay out a cash sum if youre diagnosed with or undergo a medical procedure for one of the specified critical illnesses that we cover and you survive for 14 days from diagnosis. Term the life assured.

Many of the common combined policy types include Level Term Life Insurance Critical Illness Cover as well as Decreasing Term Protection. Such as certain types of cancer. Sum assured is paid out on death during the policy term.

Simply enter the initial sum assured plan term. An insurance policy that decreases. As with all types of life insurance its possible to add critical illness cover to a decreasing-term policy but your premiums will rise to reflect this extra level of insurance.

Result in a cash sum payment of 20 of the level of critical illness cover on the plan at the time you claim or 15000 whichever is the lower. If we make an additional critical illness cover cash payment this will not reduce the amount of cover provided by your plan. This type of policy is useful for providing security for your dependents up to a certain age.

As with all Life Insurance policies you can add Critical Illness Cover to Decreasing Term Life Insurance. Group I If the person covered meets any of the conditions listed under this Group I we will pay the full sum assured less any payments already made for Total Disability if included. Like all other life insurance policies it is possible to add critical illness cover to your decreasing-term life insurance plan.

A terminal illness rider is usually included at no additional cost and allows you to access your policys death benefit while still alive if you need the funds to cover expenses such as hospice care the hiring of a caretaker or residence at a nursing home. Its often used to cover the balance of a repayment mortgage because the total balance of the mortgage decreases over time and will be paid off in full at the end of the term. Decreasing refers to the pay-out reducing over time.

Decreasing Term Assurance DTA is not an obviously self-explanatory phrase so lets break down the jargon. Theres also the option of adding a critical illness cover element to a decreasing or level term policy. NFU Mutual Financial Advisers advise on NFU Mutual products and selected products from specialist providers.

Critical illness covers you against the risk of falling seriously ill and being unable to meet your financial commitments. Decreasing term assurance can be tailored to your needs. AIG Critical Illness with Term Assurance Key Facts 5 Critical illnesses covered The critical illnesses we cover fall within three groups.

At the end of the agreed term the life assurance and critical illness cover provided by this policy will cease and this may leave you without vital cover. Critical illness insurance will cover you against falling seriously ill. Yes it is possible to take out Critical Illness Cover on a decreasing term basis.

Decreasing Term Assurance Cons. Click to open Level term assurance. Scottish Widows offer a standalone Critical Illness Cover protection policy to their customers unlike some Life insurers who only offer combined policies.

Joint life cover Your policy may cover you your partner. Payment is made if you die during the term. Sum assured decreased to reflect the outstanding loan amount each year.

Premiums stay the same though pay-out decreases. We refer to these as additional critical illness cover cash payments.

Pin On Insurance Tidbits

Pin On For Real

Life Insurance Gives You A Certainty Life Insurance Quotes Life Insurance Sales Life Insurance

Ashford Bus 323 Week 3 Discussion 1 Life Insurance Life Insurance Policy Life Insurance Life

Your Family Is Worth Getting Financially Protected Some Life Insurance Policies Can Build Ca Life Insurance Facts Life Insurance Quotes Life Insurance Sales

What Is The Survival Period In A Critical Illness Health Cover

Types Of Cover Virgin Money Life Insurance Virgin Money Uk

Insuring The Stages Of Life Life Term Life Income Protection

Term Life Insurance Lifeinsurancetips Life Insurance Facts Term Life Insurance Quotes Life Insurance Quotes

How To Layer Life Insurance To Be Most Cost Effective Term Life Life Insurance Life Insurance Policy

Critical Illness Cover Post Office

Decreasing Life Insurance Life Cover Legal General

Critical Illness Cover Legal And General

Implementing Multiple Life Insurance Policies Infographic Life Insurance Policy Life Insurance One Life

Welcome Life Insurance Policy Universal Life Insurance Term Life

Don T Make These Big Life Insurance Blunders Life Insurance Affordable Life Insurance Life Insurance Agent

Understanding Critical Illness Cover Times Money Mentor

Understanding Critical Illness Cover Times Money Mentor

Theory Of Decreasing Responsibility Life Insurance Quotes Life Insurance Marketing Life Insurance Facts

Posting Komentar untuk "Decreasing Term Assurance With Critical Illness Cover"